Abstract

This proposal seeks to incorporate a new 3% delegation fee called “DeFi-PoL” onto our existing stLINK LST smart contracts (for stLINK: from both the node operators pool and the native community pool, and once deployed for the stMETIS contracts as well, and any other LSTs we might offer in the future will follow the same delegation fee rake.

The purpose of the DeFi-PoL fee is to create a funnel for the stakedotlink DAO to have an on-chain budget in the form of its LSTs and to automatically LP it (i.e mint stLINK-LINK crv LP tokens) and distribute them as incentives to the Insurance Pool stakers who stake in the stakedotlink Reserve (formerly “Insurance Pool”), in a constant and automated way which scales in direct correlation to the protocol’s LSTs market dominance.

Note: This SLURP is in tandem and reliant on SLURP-15 - Insurance Pool - stakedotlink Reserve, as the LSTs incentives will be offered to those who stake their LP positions (UniV3,Hercules,Curve etc) into the Reserve pool. Furthermore, the initial implementation will focus on the stLINK smart contracts, and if this SLURP is approved after METIS staking is live, the DeFi-PoL fee will be funneled to a smart contract governed by the DAO, until the same implementation done for stLINK can be applied for stMETIS.

Rationale

Following our PoL temp check discussion and the Snapshot vote in favor, we agree that liquidity in secondary markets for our LSTs are a critical factor for the protocol’s success. But do we really need another fee? Our reward rate is significantly higher than native staking and will remain that way even after the DeFi PoL fee is implemented. Currently, it will decrease stLINK reward rate from 6.5% to 6.2%, which is negligible. It’s important to remember these delegation fees are “abstracted away” from the end user, which currently does not have any other existing or let alone competitive alternative.

You can play with the % differences using the calc.

Currently the TVL for the stLINK-LINK pool is $2.7M, or 111k LINK-114K stLINK. If we were to implement this fee with our current Staked Assets Under Management (stAUM) of 2.6M LINK tokens, and distribute stLINK-LINK crv LP tokens to our crv LPers (which staked their own LP tokens in the Reserve pool), they would be getting a yearly reward rate of 2.46% in the form of 50/50 LP position. Keep in mind, this is LINK rewards, not SDL. 2.46% is a considerable reward rate.

Onchain flow

The fee is taken as stLINK from the native pools reward rate, transferred to a smart contract that deposits them to the Curve pool, single sided, receiving stLINK-LINK LP tokens. These LP tokens are then deposited into our future Insurance pool(“stakedotlink Reserve”), and is distributed the same way SDL emission does to that pool’s LPs, all done via our frontend. It’s worth noting that this builds liquidity automatically over time and won’t require LP action. Besides increasing the liquidity in proportion to our stLINK mints, this could help us decrease our reliance on SDL tokens from our treasury as emission, and shift towards reward rate that is based on the protocol’s utility and core products.

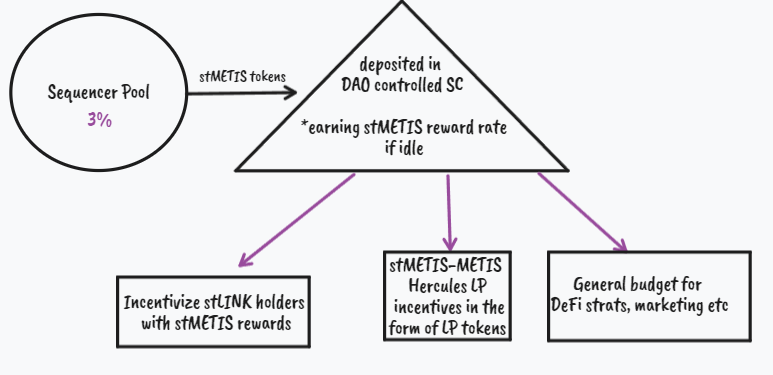

As for stMETIS, we will currently accrue the fees into a DAO controlled SC, until we create a similar funnel to stLINK.

This proposal enables stake.link to continue its natural progression towards a sustainable, viable protocol that’s prepared for the long haul.

Looking forward to ongoing discussion of SLURP-26 and encourage the community to join the conversation, ask questions, and provide their candid feedback. We’re all in this together~

Much Love,

-T.